A few years ago, I knew a person who kept saying, “I’ll buy term insurance next year.” Next year turned into another year, and then another. Life was busy. Work, bills, family responsibilities — the usual story. The problem is that life doesn’t wait for the perfect time.

That’s one reason term insurance is getting more attention in 2026.

Think about it for a second. Prices are rising almost everywhere. School fees cost more than they did a few years ago. Home loan EMIs aren’t getting any smaller. Even everyday groceries seem to surprise us when we look at the bill. If something unexpected happened to the person earning for the family, would the household still be financially stable?

That’s where a term insurance plan comes in.

It isn’t an investment scheme. It isn’t meant to make you rich. Its job is much simpler. It helps protect your family financially if you’re no longer around to support them.

Many people in India are now choosing higher coverage amounts such as ₹1 crore or more because they realize that a small policy may not be enough to cover future expenses, loans, children’s education, and daily living costs.

If you’re wondering whether you should buy term insurance in 2026, the short answer is yes—especially if anyone depends on your income. The earlier you buy, the lower your premium is likely to be. Waiting often means paying more later.

In this guide, we’ll compare the best term insurance plans in India for 2026, explain what really matters before buying, and help you choose a plan that fits your family’s needs instead of just picking the cheapest option.

What Is Term Insurance?

If you’ve ever wondered what would happen to your family’s finances if you were no longer around, that’s exactly where term insurance comes in.

In simple words, term insurance is a type of life insurance that gives your family a financial safety net if something happens to you during the policy period. You pay a premium every month or year, and in return, the insurance company promises to pay a fixed amount of money (called the sum assured) to your nominee if you pass away while the policy is active.

Think of it like a seat belt in a car.

You don’t wear a seat belt because you’re planning for an accident. You wear it because life can be unpredictable. Term insurance works in a similar way. None of us likes thinking about worst-case situations, but having a backup plan can make a huge difference for the people who depend on us.

Here’s a simple example.

Imagine you’re a 30-year-old earning ₹8 lakh a year. You have a spouse, a young child, and maybe a home loan. If something unexpected happens to you, your family’s regular income could stop overnight. A term insurance plan can provide a lump sum amount, such as ₹1 crore or more, helping them manage daily expenses, loan repayments, children’s education, and future goals without financial stress.

One thing many people don’t realize is that term insurance is usually one of the most affordable types of life insurance. Since it focuses mainly on protection and doesn’t combine investment benefits, you can often get a large life cover at a relatively low premium.

So, who should buy term insurance?

Honestly, almost anyone whose family depends on their income should consider it. Salaried employees, business owners, freelancers, self-employed professionals, parents, and even young earners who have financial responsibilities can benefit from having a term plan. The earlier you buy it, the lower your premium is likely to be.

At the end of the day, term insurance isn’t really about you. It’s about making sure the people you care about can continue their lives with dignity and financial stability, even if you’re not there to support them.

Quick Comparison Table: Best Term Insurance Plans in India 2026

If you’ve ever searched for the best term insurance plan in India, you probably know how confusing it gets.

One website says one plan is the best. Another recommends something completely different. Then an insurance agent calls and tells you a third option is perfect for you.

Honestly, I’ve seen many people spend more time choosing a smartphone than choosing life insurance. The funny thing? One decision affects your next two years. The other could affect your family’s next twenty years.

That’s why I put together this simple comparison table. Instead of looking at dozens of features you’ll never use, focus on the things that actually matter—life cover, claim settlement record, rider options, payout flexibility, and who the plan is best suited for.

Best Term Insurance Plans Comparison India 2026

| Insurance Company | Popular Term Plan | Best For | Key Riders Available | Payout Options |

|---|---|---|---|---|

| HDFC Life | Click 2 Protect Super | Families looking for flexible coverage | Critical Illness, Waiver of Premium, Accidental Death Benefit | Lump sum, monthly income, combination |

| Axis Max Life | Smart Secure Plus Plan | Young professionals and salaried employees | Critical Illness, Disability Rider, Premium Waiver | Lump sum and monthly income |

| Tata AIA Life | Sampoorna Raksha Supreme | People wanting extensive customization | Critical Illness, Accidental Death, Income Benefit | Multiple payout choices |

| ICICI Prudential | iProtect Smart | Individuals seeking comprehensive protection | Critical Illness, Terminal Illness, Disability Cover | Lump sum and income options |

| SBI Life | eShield Next | Budget-conscious buyers | Accidental Death Benefit, Critical Illness | Flexible payout modes |

| LIC | Tech Term Plan | Buyers who trust LIC’s long-standing reputation | Limited rider options | Primarily lump sum payout |

Now, before you look at the table and immediately pick the cheapest premium, slow down for a second.

A low premium is great. We all like saving money. But term insurance isn’t like buying a T-shirt during a sale.

Imagine a 30-year-old father buying a ₹1 crore term plan. One insurer charges ₹900 per month while another charges ₹1,050. The difference is just a few cups of tea every month. Yet the second plan may offer better riders, more payout flexibility, or stronger support during claim settlement.

That’s why I always tell people to compare the entire package, not just the premium.

Another thing many buyers miss is riders. Think of riders as add-on safety nets. A critical illness rider, for example, can provide financial support if you’re diagnosed with a serious medical condition such as cancer, heart disease, or kidney failure. When medical bills start piling up, that extra protection can make a huge difference.

And then there’s the payout option.

Some families prefer receiving the entire claim amount at once. Others feel more comfortable getting a monthly income that replaces the breadwinner’s salary. Neither option is right or wrong. It depends on your family’s financial habits.

The truth is, there isn’t one “best” term insurance plan in India for everyone. A plan that works perfectly for a 25-year-old software engineer in Hyderabad may not be the right fit for a 42-year-old business owner with a home loan and two school-going kids.

The best term insurance plan in India 2026 is the one that gives your family enough financial protection, fits comfortably within your budget, and provides peace of mind when life takes an unexpected turn.

Best Term Insurance Plans in India 2026

If you’ve ever searched for the best term insurance plan in India, you probably noticed something strange.

Every company claims they have the “best” plan.

One website says buy this plan. Another recommends something completely different. After 20 minutes, most people end up more confused than when they started.

I’ve seen friends spend weeks comparing policies only to realize they were focusing on the wrong things. They looked at who had the cheapest premium but ignored claim settlement history, riders, and coverage options.

The truth is pretty simple.

There isn’t one perfect term insurance plan for everyone.

A 25-year-old software engineer earning ₹8 lakh a year has different needs than a 40-year-old business owner with two kids and a home loan. That’s why instead of searching for the single “best” plan, it’s smarter to find the plan that fits your life.

Let’s look at some of the most popular term insurance plans in India for 2026 and who they may suit best.

HDFC Life Click 2 Protect Super

HDFC Life has been one of the most recognized names in the insurance industry for years.

The Click 2 Protect Super plan is popular because it gives flexibility. You can choose different payout options, add riders, and customize coverage based on your family’s needs.

One thing many buyers like is the Life Stage Benefit option. Imagine you’re 28 today and unmarried. Five years later you get married. Then a few years after that, you have a child.

Your responsibilities grow.

Instead of buying a completely new policy, this feature allows you to increase your coverage at major life events.

That’s a pretty practical option because life rarely stays the same for 30 or 40 years.

Best for: Young professionals, newly married couples, and people expecting family responsibilities to increase over time.

ICICI Prudential iProtect Smart

Whenever term insurance discussions happen, ICICI Prudential almost always appears on the list.

The iProtect Smart plan stands out because it offers more than just death coverage. It also includes options related to critical illnesses and disabilities.

Many people don’t think about this when buying insurance.

They imagine the worst-case scenario is death.

But sometimes a serious illness can affect a family’s finances even more. Medical bills start piling up while income may stop completely.

That’s where additional protection can make a difference.

A friend of mine bought a term plan after becoming a father. What convinced him wasn’t the life cover. It was knowing that a major illness wouldn’t completely destroy his savings.

That peace of mind mattered more than saving a few hundred rupees on premiums.

Best for: Families looking for broader protection beyond basic life insurance.

Tata AIA Sampoorna Raksha Supreme

Tata is a name most Indians already trust.

Whether it’s salt, tea, steel, or insurance, people generally feel comfortable dealing with the brand. That trust factor alone brings many buyers to Tata AIA.

The Sampoorna Raksha Supreme plan offers several customization options and rider combinations.

One thing many policyholders appreciate is the flexibility in payout methods. Your family can receive a lump sum amount, regular monthly income, or a combination of both.

Think about it.

If someone suddenly receives ₹1 crore, managing that money wisely may not be easy during an emotional period. Some families prefer a monthly income because it feels more predictable and easier to handle.

There isn’t a right or wrong choice here. It depends on how your family manages finances.

Best for: People who want flexible payout choices and long-term family income planning.

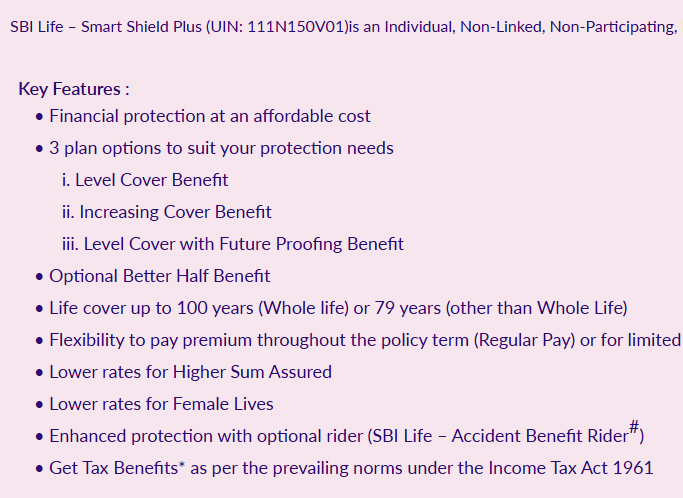

SBI Life eShield Next

SBI Life benefits from something very few insurance companies have.

Recognition in almost every corner of India.

Even people living in smaller towns and villages are familiar with SBI. That familiarity creates confidence, especially for first-time insurance buyers.

The eShield Next plan offers various coverage options, including increasing cover and level cover variants.

Many home loan borrowers find this useful.

For example, if you’re paying a home loan for the next 20 years, you may want insurance coverage that matches your financial responsibilities during that period.

The plan is also often considered by people who prefer dealing with well-known and established institutions.

Best for: Home loan borrowers and first-time insurance buyers looking for a familiar brand.

Axis Max Life Smart Secure Plus Plan

Axis Max Life has become a favorite among many online insurance buyers.

The company focuses heavily on term insurance and often receives attention because of its strong claim settlement performance and product flexibility.

One feature people frequently discuss is the ability to enhance coverage through optional benefits and riders.

When you’re young and healthy, insurance premiums are usually much lower.

A lot of people postpone buying insurance because they think they can do it later.

I understand the temptation.

When you’re 26 and healthy, insurance isn’t exactly exciting.

But every year of delay generally means higher premiums. Sometimes health conditions can appear unexpectedly and affect eligibility as well.

That’s why many financial planners suggest buying term insurance early, even before you feel like you need it.

Best for: Young earners looking for long-term affordable coverage.

LIC Tech Term Plan

For many Indians, life insurance and LIC almost feel like the same thing.

Parents trust it. Grandparents trust it. Entire families have been buying LIC products for decades.

The LIC Tech Term Plan is one of LIC’s pure term insurance offerings.

People who choose LIC usually aren’t looking for flashy features. They’re looking for reliability and familiarity.

There’s a certain comfort that comes from dealing with a brand that has been around for generations.

Of course, buyers should still compare premiums, benefits, and riders with private insurers before making a decision.

Trust is important.

But so is value.

The smartest buyers compare both.

Best for: Traditional investors who prefer established government-backed institutions.

Which Term Insurance Plan Is Best for ₹1 Crore Coverage?

This is probably the most common question people ask.

The answer depends on your age, health condition, smoking habits, occupation, and policy term.

A healthy 25-year-old non-smoker may get ₹1 crore coverage at a surprisingly affordable premium.

A 40-year-old smoker may pay several times more for the same protection.

That’s why comparing premiums alone doesn’t tell the full story.

Instead, compare:

- Claim settlement history

- Coverage options

- Critical illness benefits

- Accidental death riders

- Premium affordability

- Payout flexibility

- Company reputation

- Customer service experience

Those factors often matter far more over the next 30 years than saving a few hundred rupees annually.

My Take

If I had to give one practical suggestion, it would be this:

Don’t buy a term insurance plan just because someone on YouTube recommended it.

Don’t buy it because your friend bought it either.

Look at your income. Think about your family’s future. Calculate your loans, monthly expenses, children’s education costs, and long-term responsibilities.

Then choose a plan that can realistically protect those goals if something unexpected happens.

At the end of the day, the best term insurance plan in India for 2026 isn’t necessarily the cheapest one.

It’s the one that allows your family to continue living with dignity and financial security even when you’re no longer there to support them.

Read More: How to Lead Your Life in this AI World?

How to Choose the Best Term Insurance Plan in India

I’ll be honest. Most people spend more time comparing smartphones than comparing term insurance plans.

A phone may last 3 or 4 years. A term insurance policy could protect your family for 30 or 40 years.

That’s why choosing the right plan matters.

The problem is that many insurance websites throw around terms like claim settlement ratio, solvency ratio, riders, exclusions, and payout options. For someone buying insurance for the first time, it can feel like reading a different language.

The good news? You don’t need to be a finance expert. You just need to know a few things before clicking the “Buy Now” button.

Don’t Choose a Plan Just Because It’s Cheap

This is probably the biggest mistake people make.

Imagine two insurers offering ₹1 crore coverage. One costs ₹700 per month, while the other costs ₹850.

Many buyers immediately pick the cheaper option.

But hold on.

That extra ₹150 might give you better rider options, more flexible payouts, stronger customer service, or a better track record of settling claims. Insurance isn’t like buying a T-shirt where the cheapest option often works fine.

When your family may depend on that money someday, quality matters.

I usually tell people to compare value, not just price.

Check the Claim Settlement Ratio

You’ll hear this term everywhere.

Claim Settlement Ratio (CSR) tells you how many claims an insurance company settled out of the total claims it received during a year.

For example, if an insurer receives 100 claims and settles 98 of them, its claim settlement ratio is 98%.

Simple enough.

A high ratio generally shows that the insurer has a strong history of honoring claims. While no single number should decide your choice, I personally feel more comfortable with insurers that consistently maintain high claim settlement records over several years.

One year’s data can look impressive. A long-term pattern tells a better story.

Look at the Amount Settlement Ratio Too

Many people don’t even know this metric exists.

The claim settlement ratio shows the number of claims settled.

The Amount Settlement Ratio (ASR) shows how much money the insurer actually paid compared to the amount claimed.

Why does this matter?

Because settling a large number of small claims is different from settling high-value claims.

A company with a healthy amount settlement ratio gives you another layer of confidence that it pays substantial claim amounts when needed.

Think of CSR and ASR as two pieces of the same puzzle. Looking at both gives a clearer picture.

Check the Solvency Ratio

This sounds complicated, but it’s actually pretty straightforward.

The solvency ratio measures the financial strength of an insurance company.

In simple terms, it shows whether the insurer has enough financial resources to meet future claim obligations.

A financially strong company is generally in a better position to handle claims even during difficult economic situations.

Most people ignore this number completely. I wouldn’t make it the deciding factor, but it’s definitely worth checking before buying a long-term policy.

After all, you’re trusting this company with your family’s future for decades.

Understand What the Policy Does NOT Cover

Nobody likes reading fine print.

I get it.

But skipping exclusions can create serious problems later.

Every term insurance policy comes with situations where claims may be rejected. These exclusions vary slightly between insurers.

For example, incorrect information in the application, hiding smoking habits, undisclosed medical conditions, or certain policy-specific exclusions can lead to complications during claim processing.

This is why honesty during the application process is so important.

A friend once told me he was thinking of hiding his smoking habit to save money on premiums. I told him that saving a few hundred rupees now isn’t worth risking a claim worth ₹1 crore later.

He agreed.

Also know How to Lower Car Insurance.

Choose Useful Riders, Not Every Rider

Insurance companies love offering add-ons.

These are called riders.

Some riders are genuinely useful. Others may simply increase your premium without adding much value.

The most commonly considered riders include:

- Critical Illness Rider

- Accidental Death Benefit Rider

- Disability Rider

- Waiver of Premium Rider

For example, if you’re the only earning member in your family, a critical illness rider can provide additional financial support during a major health crisis.

But don’t fall into the trap of adding every rider available.

Ask yourself one question:

“Will this rider solve a real financial problem for my family?”

If the answer is no, skip it.

Choose the Right Coverage Amount

A ₹50 lakh policy may sound like a huge amount today.

But will it be enough after 20 years?

Maybe not.

A common rule many financial planners use is having life cover equal to 10 to 15 times your annual income.

If you earn ₹10 lakh per year, you may consider coverage between ₹1 crore and ₹1.5 crore.

Then add any major liabilities such as:

- Home loan

- Car loan

- Personal loan

- Children’s future education expenses

The goal isn’t to make your family rich.

The goal is to make sure they don’t struggle financially if you’re no longer around.

Look at Payout Options Carefully

Many modern term insurance plans offer different payout methods.

Some provide a lump sum payment.

Others offer a monthly income option.

Some combine both.

There isn’t one perfect choice for everyone.

A lump sum may work well for financially disciplined families. Monthly income options can help families that prefer a regular stream of money.

Think about how your family manages finances before choosing.

Buy Early If Possible

One thing I’ve noticed over the years is that people often delay buying term insurance.

They say things like:

“I’ll buy it next year.”

Or,

“I’ll wait until my salary increases.”

The problem is that premiums generally rise with age.

Your health can also change unexpectedly.

Buying earlier usually means lower premiums and easier approval.

Sometimes the best time to buy term insurance isn’t when you think you’re ready.

It’s when you realize your family depends on you.

A Simple Checklist Before You Buy

Before finalizing any term insurance plan, ask yourself:

✔ Does the insurer have a strong claim settlement record?

✔ Is the amount settlement ratio healthy?

✔ Is the company financially strong?

✔ Have I understood the exclusions?

✔ Am I choosing only useful riders?

✔ Is the coverage enough for my family’s future needs?

✔ Have I disclosed all health and lifestyle details honestly?

✔ Does the premium comfortably fit my budget?

If you can answer “yes” to most of these questions, you’re probably looking at a term insurance plan that deserves serious consideration.

How Much Cover Do You Need?

This is probably the biggest question people ask before buying term insurance.

And honestly, it’s a good question.

Many people simply choose a ₹50 lakh or ₹1 crore cover because a friend suggested it or because they saw it in an advertisement. I’ve seen people do that all the time. The problem is that term insurance isn’t about buying a random number. It’s about making sure your family can continue their life comfortably if you’re no longer around.

A simple rule that financial experts often recommend is buying coverage worth 10 to 15 times your annual income.

For example, if you earn ₹10 lakh a year, a cover of ₹1 crore to ₹1.5 crore may be a reasonable starting point. But that’s only the beginning. Your personal situation matters much more than any formula.

Think about your family’s monthly expenses.

Would your spouse be able to manage household costs without your income? What about your children’s school fees, college education, daily bills, groceries, and medical expenses? These things don’t stop just because life takes an unexpected turn.

Then there are loans.

Let’s say you still have a home loan of ₹40 lakh and a car loan of ₹5 lakh. If something happens to you, those liabilities don’t magically disappear. The burden may fall on your family. That’s exactly what term insurance is designed to prevent.

I usually tell people to sit down with a notebook and write three things:

- Outstanding loans

- Future family expenses

- Long-term goals like children’s education or marriage

Once you see those numbers on paper, the required coverage becomes much clearer.

Here’s a simple example.

Imagine Raj is 32 years old and earns ₹12 lakh per year. He has a wife, one young daughter, and a home loan of ₹35 lakh.

His family spends around ₹50,000 every month. He also wants to make sure his daughter can attend college without financial stress in the future.

In Raj’s case, a ₹2 crore cover may make much more sense than a ₹1 crore cover. The extra protection could make a huge difference over the next 15 or 20 years.

Another thing many people forget is inflation.

The cost of living keeps rising. A monthly expense of ₹40,000 today may easily become ₹70,000 or more years from now. Education costs seem to rise even faster. Just look at college fees compared to what they were ten years ago. The difference can be shocking.

That’s why choosing the cheapest cover isn’t always the smartest decision.

Sometimes spending a few hundred rupees more each month can significantly increase the protection your family receives.

If you’re young, married, have children, or have loans, don’t underestimate your insurance needs. Buying too little cover is one of the most common mistakes people make.

A good way to think about it is this:

Your term insurance should be large enough to replace your income, clear your debts, and help your family achieve their future goals without financial hardship.

When in doubt, it’s usually safer to choose slightly higher coverage than to discover years later that your family’s protection isn’t enough.

Best Term Insurance Plan by Buyer Type

One thing I learned after looking at dozens of term insurance plans is that there isn’t one “best” plan for everyone.

A 25-year-old software engineer doesn’t need the same policy as a 40-year-old business owner with a home loan and two kids. That’s why choosing a term insurance plan based on your life situation makes much more sense than simply picking the cheapest premium you can find.

Let’s look at what works best for different types of buyers.

Best Term Insurance Plan for Salaried Employees

If you’re working in a private company or government job and your family depends on your monthly income, term insurance is almost a necessity.

Think about it for a second. Your salary pays for rent or EMI, groceries, children’s education, utility bills, and dozens of small expenses that nobody notices until the money stops coming in.

For salaried people, a term plan with a cover amount of at least 10 to 15 times annual income is usually a good starting point.

For example, if you earn ₹10 lakh per year, a life cover of ₹1 crore to ₹1.5 crore may provide better protection for your family.

Look for:

- High claim settlement ratio

- Affordable long-term premium

- Critical illness rider

- Accidental death benefit rider

- Monthly income payout option

Many salaried employees make the mistake of relying only on employer-provided insurance. The problem is simple. If you change jobs or lose your job, that coverage often disappears.

Your personal term insurance stays with you regardless of where you work.

Best Term Insurance Plan for Self-Employed People

Business owners, freelancers, consultants, shop owners, and professionals face a slightly different challenge.

Income may not be the same every month.

Some months feel great. Other months can be surprisingly slow.

Because of this uncertainty, self-employed individuals should focus on higher protection and flexible payout options.

A friend who runs a small digital marketing agency once told me something interesting. He said his family knows his business earns money, but nobody else can run it exactly the way he does.

That is true for many entrepreneurs.

If the business depends heavily on one person, term insurance becomes even more valuable.

Things to consider:

- Larger life cover

- Long policy term

- Income replacement benefits

- Critical illness protection

- Waiver of premium rider

When applying, keep your income documents and tax returns ready. Insurers often ask for additional proof of income for self-employed applicants.

Best Term Insurance Plan for Women

More women are buying term insurance today than ever before, and honestly, that’s a good thing.

Many women contribute significantly to family finances. Some are primary earners. Others run businesses or support household expenses while raising children.

A term insurance plan can help protect those who depend on them financially.

Women also have an advantage that many people don’t realize.

Since women generally have a longer life expectancy, insurers often offer lower premiums compared to men of the same age and health condition.

Women may consider:

- Child education protection

- Critical illness rider

- Cancer cover rider

- Income payout options

- Long-term protection until retirement

If you’re buying insurance in your twenties or early thirties, premiums are usually much lower than waiting another ten years.

Best Term Insurance Plan for NRIs

Many Indians working abroad still have financial responsibilities back home.

Parents may depend on them. There could be a home loan in India. Some are saving for children’s future education or family goals.

That’s where term insurance for NRI buyers becomes useful.

Most major insurers allow eligible Non-Resident Indians to purchase term insurance plans either online or through specific application processes.

The exact requirements depend on the country of residence and insurer guidelines.

Before buying, check:

- Countries covered by the insurer

- Medical examination requirements

- Premium payment options

- Claim process for overseas families

- Currency and banking requirements

A lot of NRIs assume life insurance from their foreign employer is enough. Sometimes it is. Sometimes it isn’t. The coverage may stop when employment ends, which is why many people still maintain a separate term insurance plan in India.

Best Term Insurance Plan for Home Loan Borrowers

Buying a home feels exciting until you see the size of the EMI.

I still remember a friend joking that his house owned him more than he owned the house.

Funny, but not completely wrong.

If you have a large home loan, term insurance can prevent that financial burden from falling on your family.

Imagine a person with a ₹60 lakh or ₹1 crore loan. If something unexpected happens, the family may struggle to continue EMI payments.

A properly chosen term plan can help cover that risk.

Look for:

- Coverage matching loan amount

- Long policy term

- Increasing life cover option

- Monthly income benefits

- Joint financial planning with spouse

Many financial planners recommend combining family protection needs and outstanding loans while calculating coverage.

Best Term Insurance Plan for Young Earners

If you’re in your twenties and just started earning, term insurance probably isn’t the first thing on your mind.

Most people think about phones, bikes, travel plans, investments, or maybe a car.

Insurance feels boring.

I felt the same way when I first started learning about personal finance.

But here’s the thing.

The younger you are, the cheaper term insurance usually becomes.

A healthy 25-year-old non-smoker can often lock in a very low premium for decades. Waiting until your mid-thirties may mean paying much more for the same coverage.

Young earners should focus on:

- Early policy purchase

- High cover at low premium

- Long policy duration

- Future family protection

- Optional critical illness rider

Even if you don’t have many responsibilities today, life changes quickly. Marriage, children, loans, and family commitments often arrive sooner than expected.

Riders to Consider Before Buying a Term Insurance Plan

When people buy term insurance, most of their attention goes to the life cover amount. They compare premiums, look at claim settlement ratios, and check which company is offering the cheapest plan.

I get it. That’s what I did when I first started learning about insurance too.

But after spending time understanding how these policies actually work, I realized something important. The basic term plan only pays your family if you pass away during the policy term. Life, unfortunately, doesn’t always follow that script.

Sometimes people survive serious illnesses but struggle financially for years. Sometimes an accident leaves someone unable to work. That’s where riders can make a big difference.

Think of riders as optional add-ons that give your policy extra protection.

Critical Illness Rider

This is probably one of the most useful riders for many families.

Imagine you’re 35 years old, have a home loan, two kids, and suddenly get diagnosed with cancer or suffer a major heart attack. Medical treatment can cost lakhs of rupees. At the same time, your income may stop or reduce.

A critical illness rider pays a lump sum amount if you’re diagnosed with a covered illness listed in the policy.

The money can be used for treatment, household expenses, loan EMIs, or anything else you need.

I’ve seen people focus only on life cover and completely ignore the financial impact of a serious illness. Honestly, that’s a mistake. For many working professionals, this rider is worth considering.

Accidental Death Benefit Rider

Life insurance already covers death, so some people wonder why they need this rider.

The difference is simple.

If death happens because of an accident, this rider provides an additional payout on top of the regular life cover.

Let’s say your base term insurance cover is ₹1 crore. If you have an accidental death rider of ₹50 lakh and an accident causes death, your family could receive ₹1.5 crore instead of ₹1 crore.

If you travel frequently, drive long distances, work in construction, manufacturing, or any occupation with higher physical risk, this rider may offer extra peace of mind.

Waiver of Premium Rider

This rider doesn’t get enough attention, yet it can be extremely valuable.

Picture this.

A person suffers a permanent disability after an accident and can no longer work. Income drops. Household expenses continue. School fees continue. Loan EMIs continue.

Paying insurance premiums may become difficult.

With a waiver of premium rider, future premiums are waived under certain conditions, but the policy continues. In simple words, you don’t lose your insurance cover even if you’re unable to pay premiums because of a covered disability or illness.

For someone who is the primary earning member of the family, this rider can be a lifesaver.

Disability Rider

Many people think about death but rarely think about disability.

The truth is, a severe disability can affect a family’s finances just as much as death, sometimes even more.

A disability rider provides financial support if an accident leads to permanent total disability or, in some policies, partial disability.

The benefit may come as a lump sum payment, monthly income, or a combination of both, depending on the insurer and policy terms.

If your family depends mainly on your income, this rider deserves serious consideration.

Do You Need Every Rider?

Not necessarily.

This is where many buyers go wrong. They add every available rider without asking whether they actually need it.

More riders mean higher premiums.

A better approach is to think about your personal situation.

- If you have dependents and worry about expensive medical treatments, consider a critical illness rider.

- If your work or travel increases accident risk, look at an accidental death benefit rider.

- If your family relies heavily on your income, waiver of premium and disability riders can provide valuable protection.

The goal isn’t to collect riders like mobile app subscriptions. The goal is to protect yourself against risks that could seriously affect your family’s finances.

A good term insurance plan is not always the cheapest one. It’s the one that protects your family when life takes an unexpected turn. And sometimes, the right rider can make all the difference.

Term Insurance vs Return of Premium (ROP): Which One Makes More Sense?

This is one of the most common questions people ask when buying a term insurance plan.

“Why should I pay premiums for 30 or 40 years and get nothing back if I survive?”

Honestly, I used to think the same way.

At first glance, a Return of Premium (ROP) plan sounds like a better deal. After all, if you live through the policy term, the insurance company returns the premiums you paid. It feels like you’re getting something back for your money.

But once you look a little deeper, things become more interesting.

What Is a Regular Term Insurance Plan?

A regular term insurance plan is simple.

You pay a premium every year. If something happens to you during the policy period, your family receives the sum assured. If you outlive the policy term, there is no maturity benefit.

Many people see this as a drawback. But that’s not always fair.

Think about your car insurance. You don’t expect the insurer to return all your premiums because you didn’t have an accident. You buy it for protection. Term insurance works in a similar way.

Its main job is to protect your family’s financial future.

What Is a Return of Premium (ROP) Plan?

A Return of Premium plan works differently.

If you survive the policy term, the insurer returns the base premiums you paid over the years. That sounds comforting, especially for first-time buyers who don’t like the idea of “losing” money.

For example, imagine you pay ₹20,000 every year for 30 years.

At the end of the policy term, you may receive the total premiums paid back, depending on the policy terms.

Seems attractive, right?

Well, there’s a catch.

Why Is Regular Term Insurance Usually Cheaper?

The biggest difference is cost.

A regular term plan can be significantly cheaper than a Return of Premium plan for the same life cover.

Let’s say a 30-year-old non-smoker wants ₹1 crore coverage.

A pure term plan might cost around ₹10,000–₹15,000 per year. An ROP plan could easily cost much more for the same protection.

Over decades, that extra amount adds up.

Many financial planners prefer buying a simple term plan and investing the savings separately. If those investments grow well, the final amount may be higher than the premium refund from an ROP policy.

Of course, investing requires discipline. That’s where some people struggle.

When Does a Return of Premium Plan Make Sense?

ROP isn’t a bad product.

It may suit you if you know you’ll feel disappointed receiving nothing at maturity. Some people value peace of mind more than maximizing returns.

It can also work for those who want insurance and a guaranteed refund without worrying about stock markets, mutual funds, or investment decisions.

I’ve met people who sleep better knowing they’ll at least get their premiums back someday. And that’s perfectly okay.

Personal finance isn’t only about numbers. Emotions matter too.

So, Which One Should You Choose?

If your goal is getting the highest life cover at the lowest possible cost, a regular term insurance plan is usually the better option.

If you want a maturity benefit and don’t mind paying higher premiums, a Return of Premium plan may fit your comfort level.

The real mistake isn’t choosing one over the other.

The real mistake is delaying insurance while trying to find the “perfect” plan.

A good policy purchased today is often far better than spending years comparing options and buying nothing at all.

Read More: Best Health Insurance Plans for Family in India 2026.

Online vs Offline Term Insurance: Which One Should You Choose?

A few years ago, buying insurance usually meant sitting across a desk from an agent, listening to policy details, signing papers, and hoping you understood everything correctly. Things have changed a lot since then. Today, you can buy a term insurance plan from your phone while sitting on your couch with a cup of tea in your hand.

But does that mean online term insurance is always better?

Not necessarily.

The right choice depends on what kind of buyer you are.

Online Term Insurance

Online term insurance is purchased directly through the insurance company’s website or a trusted insurance marketplace. There is no middleman involved, which is one reason why online plans are often cheaper.

For example, a 30-year-old healthy non-smoker may find that the same ₹1 crore term plan costs a little less online than through an agent. Over a policy period of 30 or 40 years, even a small difference in premium can add up to a significant amount.

Another thing I like about online buying is transparency. You can compare different insurers, check policy features, read exclusions, and calculate premiums at your own pace. Nobody is rushing you to make a decision.

The downside? You’re on your own.

If insurance terms like “sum assured,” “waiver of premium,” or “critical illness rider” sound confusing, you may spend hours researching before feeling comfortable enough to buy.

Offline Term Insurance

Offline term insurance is purchased through an insurance agent, financial advisor, or branch office.

For many people, especially first-time buyers, having a real person explain things can be reassuring. My uncle bought his first insurance policy through an advisor because he simply didn’t trust clicking a few buttons online for something that would protect his family for decades.

A good agent can help you understand policy features, fill out forms correctly, schedule medical tests, and answer questions whenever you need support.

That said, the experience depends heavily on the person you’re dealing with.

Some advisors genuinely help customers choose the right coverage. Others may focus more on selling plans that offer them higher commissions. That’s why it’s important to ask questions and never buy a policy just because someone says it’s “the best.”

So, Which Is Better?

If you’re comfortable comparing plans, reading policy documents, and making decisions yourself, online term insurance is usually the more affordable and convenient option.

If you’re completely new to insurance, have complex financial needs, or simply prefer human guidance, offline buying may give you more confidence.

The truth is, the policy itself matters far more than the purchase method.

Whether you buy online or offline, pay attention to the insurer’s claim settlement record, policy features, riders, exclusions, premium affordability, and the amount of coverage your family would actually need if something happened to you.

At the end of the day, the best term insurance plan isn’t the one bought online or offline. It’s the one that your family can depend on when they need it most.

Common Term Insurance Mistakes to Avoid

Buying a term insurance plan sounds simple. You compare a few plans, pay the premium, and feel relieved that your family is protected.

But here’s the thing. A lot of people make small mistakes while buying term insurance. Those mistakes don’t seem like a big deal today. Years later, though, they can create serious problems for the family the policy was supposed to protect.

I’ve seen many people spend hours comparing premiums but only a few minutes understanding the actual policy. That’s where trouble usually starts.

1. Buying Too Little Coverage

This is probably the most common mistake.

Many people choose a cover amount based on what feels affordable instead of what their family would actually need if something happened to them.

Imagine you earn ₹10 lakh a year and have a home loan, children’s education expenses, and daily household costs. Buying a ₹25 lakh cover just because the premium is cheap may not help your family for very long.

A simple rule many financial experts suggest is choosing coverage worth at least 10 to 15 times your annual income. Your debts, future goals, and family responsibilities should also be considered.

It might cost a few hundred rupees more each month, but that extra protection can make a huge difference.

2. Hiding Health Problems or Smoking Habits

I understand why some people do this.

When the insurance form asks whether you smoke, drink regularly, or have a medical condition, there’s a temptation to click “No” and move on. After all, nobody wants higher premiums.

The problem is that insurance companies verify information during claim investigations. If they discover that important details were hidden, the claim can become complicated or even rejected in certain situations.

Always tell the truth.

If you smoke occasionally, mention it. If you have diabetes, high blood pressure, or any existing medical issue, disclose it clearly. Paying a slightly higher premium is far better than leaving your family with uncertainty later.

3. Choosing Only the Cheapest Plan

We all like saving money. That’s normal.

But term insurance shouldn’t be treated like buying the cheapest phone charger online.

A low premium looks attractive, but it shouldn’t be the only factor you consider. Look at the insurer’s claim settlement record, customer service reputation, available riders, and overall financial strength.

Sometimes the difference between two plans is only a few hundred rupees per year. Yet the overall benefits can be very different.

A cheap plan isn’t always a bad plan. Just don’t make price your only decision-maker.

4. Ignoring Nominee Details

This sounds like a tiny thing, but you’d be surprised how many people overlook it.

Some people forget to add a nominee. Others enter incorrect details or never update the nominee after marriage, divorce, or major family changes.

Years later, when a claim needs to be settled, these mistakes can create unnecessary paperwork and delays.

Take a few minutes to review your nominee information. Make sure names, dates of birth, and relationships are correct. If your family situation changes, update the policy.

It’s one of those boring tasks nobody enjoys doing, but it matters.

5. Waiting Too Long to Buy a Policy

Many people think term insurance is something they’ll buy “next year.”

Then next year becomes the year after that.

Meanwhile, age increases, premiums rise, and health conditions may develop. A plan that costs very little at age 25 can cost significantly more at age 35 or 40.

I often tell friends this: the best time to buy term insurance is when you think you don’t need it yet.

Young and healthy applicants usually get the lowest premiums and the easiest approval process.

6. Not Reading the Policy Properly

Let’s be honest.

Most people don’t enjoy reading insurance documents. The language can feel dry and confusing.

Still, spending thirty minutes understanding your policy can save your family from future surprises.

Pay attention to exclusions, waiting periods, payout options, policy term, and rider conditions. If something isn’t clear, ask questions before buying.

Never assume. Insurance is too important for assumptions.

7. Forgetting to Add Useful Riders

A basic term plan provides life cover. That’s great, but sometimes additional protection can be valuable.

For example, a critical illness rider may help if you’re diagnosed with a serious medical condition. A waiver of premium rider can keep the policy active even if you’re unable to earn due to disability.

Not everyone needs every rider. But ignoring them completely without understanding their benefits isn’t a smart move either.

Final Thought

Term insurance is one of the simplest financial products you’ll ever buy, yet many people make it more complicated than necessary.

Choose enough coverage. Be honest about your health. Don’t chase the lowest premium blindly. Keep nominee details updated. And buy the policy before age and health start working against you.

A few careful decisions today can protect your family for decades. That’s really what term insurance is all about.

Documents Required and Term Insurance Buying Process

One thing that surprises many people is how easy it has become to buy term insurance today. A few years ago, it felt like a long and tiring process with piles of paperwork. Now, most insurance companies let you complete almost everything online from your phone or laptop.

Still, you’ll need a few basic documents ready before you start.

The first is your KYC documents. This usually includes your Aadhaar Card, PAN Card, passport, voter ID, or driving license. Insurance companies use these to verify who you are and where you live.

Next comes income proof. This part matters because insurers want to make sure the amount of life cover you are applying for matches your income. Depending on your job, they may ask for salary slips, bank statements, Form 16, income tax returns, or business income documents.

I remember helping a friend buy a ₹2 crore term plan. He thought only his Aadhaar and PAN card would be enough. Halfway through the application, the insurer requested his salary slips and ITR documents. The process wasn’t difficult, but having those documents ready would have saved him a few days.

Many insurers also ask you to fill out a proposal form. Don’t rush through it.

This form contains questions about your age, occupation, lifestyle habits, medical history, existing insurance policies, and family health background. Be completely honest here. If you smoke occasionally, mention it. If you have diabetes, mention that too. Some people hide health details hoping to get a lower premium. That’s a mistake that can create problems for their family later during claim settlement.

You may also be asked to undergo a medical test.

Now, don’t panic when you hear the words “medical examination.” For most people, it’s a routine health check. The insurer may check your blood pressure, blood sugar, weight, height, blood sample, urine sample, and a few other basic health indicators. In many cases, the insurance company even arranges the test at your home without charging extra.

Once your documents are verified and the medical assessment is completed, the insurer reviews your application. This stage is called underwriting. Sounds complicated, but all they’re really doing is evaluating the level of risk before approving the policy.

If everything looks good, you’ll receive the policy document and coverage starts after payment confirmation.

The whole process can take anywhere from a few hours to a few days, depending on your profile and the insurer. Honestly, the hardest part is usually gathering your documents. After that, things move pretty smoothly.

Before clicking the final “Buy Now” button, take a minute to double-check your nominee details, contact information, and policy coverage amount. It may seem like a small step today, but it can make a huge difference for your family years down the road.

Frequently Asked Questions (FAQs) About the Best Term Insurance Plan in India 2026

1. Which is the best term insurance plan in India in 2026?

There isn’t one single plan that’s perfect for everyone. The best term insurance plan is the one that gives enough coverage for your family’s needs, has a strong claim settlement record, useful riders, and a premium you can comfortably afford for many years. What works for a 25-year-old bachelor may not work for a 40-year-old parent with a home loan.

2. How much term insurance cover should I buy?

A simple rule many financial experts suggest is buying coverage worth at least 10 to 15 times your annual income. For example, if you earn ₹10 lakh a year, you may consider a cover of ₹1 crore to ₹1.5 crore. But don’t stop there. Think about your home loan, children’s education, family expenses, and future goals too.

3. Is a ₹1 crore term insurance plan enough?

For some people, yes. For others, not really.

If you’re young, have no major loans, and your family’s expenses are modest, ₹1 crore may be enough. But if you live in a metro city, have large financial responsibilities, or multiple dependents, you might need a higher cover.

4. At what age should I buy term insurance?

Honestly, the earlier, the better.

I often tell people that term insurance is one of those things that’s cheapest when you don’t feel like you need it. A healthy 25-year-old usually pays much lower premiums than someone buying the same plan at 40. Waiting often means paying more.

5. Can I buy term insurance without a medical test?

Some insurers offer policies without medical tests for certain age groups and coverage amounts. Still, medical tests can actually work in your favor if you’re healthy because they help insurers assess risk accurately.

Whatever you do, don’t hide any health information. Saving a few minutes today isn’t worth creating problems for your family later.

6. What happens if I survive the policy term?

In a regular term insurance plan, no maturity benefit is paid if you survive the policy period. The plan’s purpose is pure financial protection.

However, some insurers offer Return of Premium (ROP) plans. These return part or all of the premiums paid if you outlive the policy term. Just remember that ROP plans usually cost significantly more than standard term plans.

7. Are term insurance premiums fixed for the entire policy period?

In most cases, yes.

If you choose a level premium option, the premium remains the same throughout the policy term. That’s one reason many people prefer buying early. They can lock in a lower premium for decades.

8. Which riders should I add to my term insurance policy?

It depends on your situation, but many buyers consider:

- Critical illness rider

- Accidental death benefit rider

- Permanent disability rider

- Waiver of premium rider

Don’t add every rider just because it’s available. Pick the ones that genuinely solve a risk in your life.

9. Is term insurance better than traditional life insurance policies?

For pure protection, many financial planners believe term insurance offers better value.

A term plan provides a large cover amount at a relatively low premium. Traditional policies often combine insurance with savings or investment components, which can make them more expensive.

Many people prefer keeping insurance and investments separate, but your choice should match your financial goals.

10. Can housewives and non-working spouses buy term insurance?

Yes, in many cases they can.

Eligibility rules vary between insurers. Some companies issue policies based on the earning spouse’s income and the family’s financial profile. It’s worth checking the specific requirements before applying.

11. Will my family receive the claim if I die outside India?

Generally, yes.

Most term insurance policies provide worldwide coverage. If the policy is active and all information provided during purchase was accurate, the nominee can usually file a claim even if the policyholder passes away abroad.

Always read the policy terms carefully because conditions can vary.

12. What is the biggest mistake people make while buying term insurance?

If I had to pick just one, it would be buying too little coverage.

Many people focus only on getting the cheapest premium. A difference of a few hundred rupees per month may seem important today, but an insufficient cover amount can leave your family financially vulnerable later.

The goal isn’t to save money on the premium. The goal is to make sure your loved ones can maintain their lives even when you’re not around.

Conclusion: Which Term Insurance Is Best in India in 2026?

After comparing different plans, one thing becomes pretty clear: there isn’t a single “best” term insurance plan for everyone.

A plan that works perfectly for a 25-year-old software engineer may not be the right choice for a 40-year-old parent with a home loan and two kids. That’s why chasing the cheapest premium alone can sometimes be a costly mistake later.

If I were buying a term plan today, I’d focus on a few simple things. First, make sure the coverage amount is enough to support your family’s future. Second, check the insurer’s claim settlement record and reputation. Third, choose useful riders only if they genuinely fit your needs. And finally, read the policy details carefully before clicking the buy button.

Think of term insurance as a safety net. You hope your family never has to use it, but if life takes an unexpected turn, that policy can protect their dreams, education plans, monthly expenses, and financial stability.

Before you purchase any policy, use this quick checklist:

✔ Adequate life cover (usually 10–15 times your annual income)

✔ Honest disclosure of health and lifestyle habits

✔ Strong claim settlement history

✔ Affordable long-term premium

✔ Suitable riders if needed

✔ Correct nominee details

✔ Policy term covering your working years

The best term insurance plan in India in 2026 is simply the one that gives your family enough protection without putting pressure on your monthly budget. Don’t rush the decision. Spend a little time comparing plans today. Your future self—and your family—will be glad you did.

Leave a Reply