A single hospital bill can change a family’s finances overnight. I’ve seen people spend years building savings, only to watch a large chunk disappear after one unexpected surgery or emergency hospital stay. Nobody plans for these situations, but they happen more often than we like to think.

That’s one reason why many families are now looking for the best health insurance plans for family in India. A good family health insurance policy can cover your spouse, children, and in some cases even your parents under one plan. Instead of worrying about how you’ll pay medical bills, you can focus on what really matters—helping your loved ones recover.

The tricky part is that there are dozens of policies available. Every insurer claims their plan is the best. Premiums look different. Features vary. Waiting periods can be confusing. And honestly, insurance terms sometimes feel like they’re written in another language.

I remember helping a relative compare policies a few years ago. We thought choosing the cheapest option would save money. Later, we discovered important benefits were missing. That experience taught me that price alone doesn’t tell the whole story.

This guide is here to make things easier. You’ll learn how to compare the best health insurance policy for family India 2026, understand important features, check waiting periods, and avoid common mistakes that many buyers regret later. By the end, you’ll have a much clearer idea of which plan fits your family’s needs and budget.

What Is a Family Health Insurance Plan?

If you’ve ever looked at hospital bills in India, you already know how quickly medical costs can pile up. One unexpected surgery or a few days in a private hospital can easily eat into your savings. That’s exactly why many families choose a family health insurance plan.

A family health insurance plan is a single policy that covers more than one family member. Usually, you can include yourself, your spouse, children, and sometimes even dependent parents. Instead of buying separate policies for everyone, you get one plan that protects the whole family.

Most of these plans work as a family floater health insurance policy. That simply means all covered members share one insurance amount, known as a shared sum insured. For example, if your family floater policy has a coverage of ₹15 lakh, any insured family member can use that amount for medical expenses when needed.

I always think of it like a shared emergency fund. Nobody hopes to use it, but it’s there when life throws a surprise your way.

One thing many people don’t realize is that the premium often depends on the age of the oldest insured member. So, if you’re adding your parents to the same policy, the cost can increase quite a bit. That’s why many insurance experts suggest comparing separate plans for senior citizens before adding parents to a family floater.

In simple words, a family floater plan gives one umbrella of protection to the entire family, making health coverage easier to manage and often more affordable than buying multiple individual policies.

This version is optimized for readability, natural engagement, and SEO while naturally incorporating the target keywords without sounding forced.

Best Health Insurance Plans for Family in India: Quick Comparison Table

If you’ve ever tried comparing family health insurance plans in India, you already know how confusing it can get. One plan talks about unlimited restoration. Another promises a huge bonus every year. Then you see terms like “PED waiting period” and “room rent limit,” and suddenly you’re wondering if you need an insurance degree just to buy a policy.

I remember helping a relative choose a family floater plan a while back. We spent hours jumping between websites, brochures, and YouTube videos. Almost every plan claimed to be the “best.” The truth? There isn’t one perfect plan for everyone. The right choice depends on your family’s size, age, health conditions, and budget.

To save you some time, here’s a quick comparison of some of the most popular family health insurance plans available in India right now.

| Plan Name | Insurer | Best For | Sum Insured Options | Room Rent Limit | Restoration Benefit | PED Waiting Period* | Network Hospitals | Key Benefit | Possible Drawback |

|---|---|---|---|---|---|---|---|---|---|

| Care Supreme | Care Health Insurance | Families looking for high coverage at reasonable premiums | ₹5 Lakh – ₹1 Crore+ | No restriction | Yes | 3 Years | 11,000+ | Strong restoration and bonus benefits | Add-ons may increase premium |

| Niva Bupa ReAssure 2.0 | Niva Bupa | Families wanting extensive coverage and refill benefits | ₹5 Lakh – ₹1 Crore+ | No restriction | Unlimited refill | 3 Years | 10,000+ | Unlimited reinstatement of cover | Premium may be higher than some competitors |

| Optima Secure | HDFC ERGO | Families seeking comprehensive protection | ₹5 Lakh – ₹2 Crore | No restriction | Yes | 3 Years | 13,000+ | Coverage can grow significantly over time | Slightly expensive for larger families |

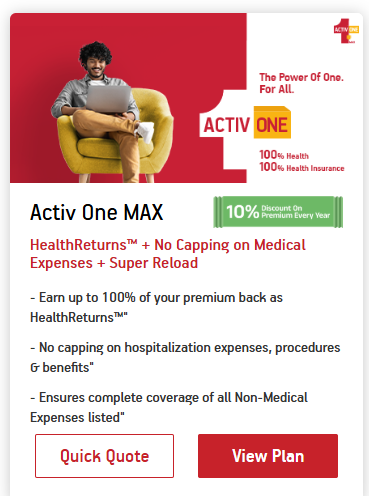

| Activ One MAX | Aditya Birla Health Insurance | Health-conscious families | ₹5 Lakh – ₹6 Crore | No restriction | Yes | 3 Years | 11,000+ | Wellness rewards and health management features | Benefits may feel overwhelming for some buyers |

| Family Health Optima | Star Health | Families looking for a trusted standalone health insurer | ₹3 Lakh – ₹25 Lakh | No major restriction | Automatic restoration | 3 Years | 14,000+ | Strong hospital network across India | Lower coverage options compared to newer plans |

| Medicare Premier | Tata AIG | Families wanting premium benefits | ₹5 Lakh – ₹3 Crore | No restriction | Yes | 3 Years | 12,000+ | High sum insured choices and global treatment options | Premiums can be on the higher side |

| Health AdvantEdge | ICICI Lombard | Urban families seeking flexible coverage | ₹5 Lakh – ₹3 Crore | No restriction | Yes | 3 Years | 9,500+ | Wide customization options | Add-ons can increase costs |

| Arogya Supreme (Family) | SBI General | Budget-focused families | ₹5 Lakh – ₹1 Crore | No restriction | Yes | 3 Years | 16,000+ | Competitive pricing and large hospital network | Fewer premium features than top-tier plans |

*PED = Pre-Existing Disease

A few plans stand out when you look beyond the marketing promises. Care Supreme has become popular because it balances coverage, features, and affordability pretty well. Niva Bupa ReAssure 2.0 is another strong option, especially if you’re worried about multiple claims in the same year since it offers powerful restoration benefits. Aditya Birla Activ One MAX also catches attention because of its wellness programs and flexible add-ons.

That said, don’t pick a plan just because it appears at the top of a comparison table. A family with two young children may need something very different from a family caring for elderly parents. Always check nearby network hospitals, waiting periods, co-pay clauses, and exclusions before making a final decision.

Health insurance isn’t exciting. Nobody sits around talking about it over dinner. But when a hospital bill suddenly lands in your hands, having the right policy can feel like one of the smartest decisions you’ve ever made.

How Much Health Insurance Cover Is Enough for a Family in India?

This is one of those questions almost every family asks before buying health insurance. And honestly, there isn’t one perfect answer for everyone.

The right sum insured depends a lot on where you live, your family’s medical history, and how expensive healthcare is in your area.

If you live in a small town, a ₹5 lakh to ₹10 lakh health insurance cover may work for many families. Hospital costs are usually lower, and routine treatments don’t drain savings as quickly.

For families living in tier-2 cities like Indore, Vijayawada, Nagpur, or Coimbatore, I feel a ₹10 lakh to ₹15 lakh family floater cover is a safer choice. Medical costs have gone up quite a bit over the last few years, and a single surgery can easily cost several lakhs.

Now, if you’re in a metro city such as Mumbai, Delhi, Bengaluru, Hyderabad, or Chennai, things get expensive fast. A few years ago, ₹5 lakh looked like a big number. Today, it can disappear surprisingly quickly after a major hospitalization. That’s why many insurance experts suggest starting with ₹15 lakh to ₹25 lakh health insurance coverage for metro families.

Think about it this way. If you have a spouse and two children under one family floater cover, the entire family shares the same insurance amount. If one member uses a large part of it, the remaining balance becomes available for everyone else.

Personally, I’d rather have a little extra coverage and sleep peacefully than save a few hundred rupees on premium and worry later. Medical emergencies rarely give us time to prepare. A good health insurance plan should.

Family Floater vs Individual Health Insurance: Which Is Better?

I’ll be honest. This is one of the most confusing parts of buying health insurance.

A lot of people see the words family floater and individual policy and assume they’re basically the same thing. I used to think that too. But after comparing plans and talking to people who actually had to make claims, I realized the difference can matter a lot when a medical emergency happens.

Let’s keep it simple.

| Feature | Family Floater Health Insurance | Individual Health Insurance |

|---|---|---|

| Coverage | One policy covers the whole family | Separate coverage for each person |

| Sum Insured | Shared among all members | Each member gets their own cover |

| Premium | Usually lower | Usually higher |

| Best For | Young couples and families with children | People with health issues or older members |

| Claim Impact | One large claim reduces available cover for others | One person’s claim doesn’t affect others |

| Flexibility | Limited | More flexible |

A family floater plan works well when everyone in the family is relatively young and healthy. The entire family shares one sum insured amount.

For example, imagine you buy a ₹15 lakh family floater policy for yourself, your spouse, and your two children. If you use ₹5 lakh for a hospital stay, the remaining ₹10 lakh stays available for the rest of the family during that policy year.

That’s why family floater plans are often cheaper. You’re sharing the coverage instead of buying separate policies for everyone.

But things can get tricky when one family member is much older or already has health problems.

Let’s say your father is 68 and has diabetes and heart issues. Adding him to your family floater may increase the premium significantly. In some cases, the insurer may apply longer waiting periods or other restrictions.

This is where an individual policy starts making more sense.

With an individual health insurance plan, every person gets their own sum insured. If your spouse makes a claim, your coverage remains untouched. That’s a big advantage when multiple family members might need medical treatment in the same year.

Personally, I think one of the smartest approaches is this:

- Buy a family floater plan for yourself, your spouse, and your children.

- Purchase separate parents health insurance or senior citizen health insurance plans for your mother and father.

Many insurance advisors recommend this approach because it keeps premiums manageable while giving older parents coverage designed specifically for their age and health needs.

So, which option wins?

If you’re a young family looking for affordable protection, a family floater vs individual policy comparison usually favors the family floater plan.

If one member is older, has ongoing medical conditions, or you’re buying coverage for parents, individual plans are often the safer choice.

At the end of the day, the best policy isn’t the cheapest one. It’s the one that still protects your family when life throws an unexpected hospital bill your way.

Key Features to Check Before Buying Family Health Insurance

Buying family health insurance can feel a bit confusing at first. Every company says their plan is the best. Every brochure is packed with fancy terms. I remember helping a relative compare different policies a few years ago, and honestly, after reading three plans, my head was spinning.

The good news? You don’t need to understand every insurance word on the planet. You just need to focus on a few features that can make a huge difference when a medical emergency actually happens.

Check the Room Rent Limit

This is one of the most overlooked things people miss.

Imagine you’re hospitalized and choose a room that costs ₹5,000 per day. Sounds reasonable, right? But if your policy allows only ₹3,000 per day room rent, you may end up paying a portion of many other hospital charges too.

That’s why I usually prefer plans with no room rent capping whenever possible. It gives you more freedom during a stressful situation. The last thing anyone wants is to argue about room categories while sitting in a hospital.

Look for a Restoration Benefit

A good restoration benefit can save your family from unexpected expenses.

Let’s say your family has a ₹10 lakh cover. One member uses most of that amount for a major surgery. A few months later, another family member needs hospitalization too.

Without restoration, your available cover may be very low.

With restoration, the insurer automatically restores the sum insured, giving your family another safety net. For families with multiple members under one policy, this feature is incredibly useful.

Don’t Ignore Pre and Post Hospitalization Cover

Most people think insurance only pays for hospital bills.

That’s not entirely true.

Before admission, doctors often recommend blood tests, scans, consultations, and medicines. Even after discharge, there may be follow-up visits, tests, and medication for several weeks or months.

A solid policy should provide pre hospitalization and post hospitalization coverage. These costs may seem small individually, but together they can add up surprisingly fast.

Day Care Procedures Matter More Than You Think

Years ago, many treatments required patients to stay in the hospital for days.

Things have changed.

Today, procedures like cataract surgery, chemotherapy sessions, dialysis, and certain minor surgeries may be completed within a few hours.

These are called day care treatments.

If your policy covers a large number of day care procedures, you’re less likely to face unpleasant surprises later. It sounds like a small detail until someone in the family actually needs one.

Check for AYUSH Coverage

A lot of families in India use traditional treatments along with modern medicine.

That’s where AYUSH coverage becomes useful.

AYUSH includes Ayurveda, Yoga, Unani, Siddha, and Homeopathy treatments. If your family prefers these treatment methods, make sure the policy covers them. Not every plan offers the same level of protection.

Maternity and Newborn Baby Cover

Young couples often skip this section because they think they’ll worry about it later.

Then later arrives much faster than expected.

If you’re planning to have children in the next few years, check whether the policy includes maternity benefits. Also look at the waiting period because many plans require you to wait before claiming maternity expenses.

A good policy may also cover your newborn baby’s medical expenses for a certain period after birth.

OPD Coverage Can Be Helpful

Not every health expense requires hospitalization.

Regular doctor visits, consultations, and small treatments can quietly drain your wallet over time.

Some premium policies offer OPD benefits that cover these expenses. It may not be a must-have for everyone, but families with young children or elderly members often find it useful.

Ambulance Coverage Is Worth Checking

Nobody plans for emergencies.

When an emergency happens, an ambulance may be needed immediately. Depending on the city and distance, ambulance charges can be surprisingly expensive.

Many good family health insurance plans include ambulance expenses. It’s a small feature, but you’ll appreciate it if you ever need it.

Annual Health Check-Ups Are a Nice Bonus

One feature I personally like is the free annual health check-up.

Many serious illnesses are easier to manage when detected early. Regular health screenings can help identify problems before they become bigger and more expensive.

Think of it as a preventive benefit rather than just an insurance feature.

Check Network Hospitals Near Your Home

This might be the most practical point of all.

A policy can have hundreds or even thousands of network hospitals across India. That sounds impressive on paper.

But here’s the real question:

Are there good network hospitals near your home, workplace, or where your parents live?

Cashless treatment becomes much easier when nearby hospitals are part of the insurer’s network. Spend a few minutes checking this before buying a policy. Future-you will probably be thankful.

Waiting Periods You Must Understand Before Buying

I still remember talking to a friend who bought health insurance and thought he was fully protected from day one. A few months later, he needed treatment and was shocked when the insurer didn’t pay the claim. The reason? A waiting period he never paid attention to.

Honestly, this happens more often than people think.

When you’re comparing family health insurance plans, don’t just look at the premium or coverage amount. Spend a few minutes understanding the waiting periods too. It can save you from a lot of frustration later.

1. The 30-Day Initial Waiting Period

Most health insurance policies come with a 30-day initial waiting period. This means you generally can’t make a claim for illnesses during the first 30 days after buying the policy.

There is one major exception, though. If you’re hospitalized because of an accident, the coverage usually starts immediately.

Think of it this way. Insurance companies want to prevent people from buying a policy only after they become sick. That’s why this waiting period exists.

2. Disease-Specific Waiting Period

Some medical conditions have their own separate waiting period. This is often called a specific waiting period.

Common examples include:

- Hernia

- Cataract

- Kidney stones

- Joint replacement surgery

- Varicose veins

Depending on the insurer and policy, the waiting period may range from one to three years.

I know that sounds like a long time. But if you already know you may need treatment for one of these conditions in the future, checking this section of the policy document becomes really important.

3. PED Waiting Period (Pre-Existing Diseases)

A PED waiting period applies to illnesses or medical conditions you already had before purchasing the policy.

For example, if you have diabetes, high blood pressure, thyroid problems, or asthma when you buy the insurance, those conditions are considered pre-existing diseases.

The good news is that health insurance rules have become more customer-friendly. Under IRDAI’s updated guidelines, insurers can keep a pre-existing disease waiting period of up to 36 months (3 years), but not longer.

That’s a big improvement compared to older policies where people sometimes had to wait four years or more.

4. Maternity Waiting Period

If you’re planning to start or expand your family, pay close attention to the maternity waiting period.

Many family health insurance plans cover pregnancy-related expenses, but not immediately. Most policies require you to wait anywhere between 9 months and 4 years before maternity benefits become available.

I’ve seen couples buy insurance after finding out they’re expecting a baby, only to discover that maternity expenses aren’t covered because the waiting period hasn’t been completed.

It’s one of those details that’s easy to miss until you actually need it.

What About the Moratorium Period?

You may also come across the term moratorium period while reading policy documents.

In simple words, once you’ve continuously maintained your policy for a specified period and disclosed your medical information honestly, the insurer generally cannot question older disclosed health conditions except in cases of fraud or misrepresentation.

Most people never pay attention to this clause, but it provides valuable long-term protection for policyholders.

At the end of the day, waiting periods aren’t exciting to read about. I get it. Most of us skip the fine print and jump straight to the coverage amount.

But a health insurance policy is only useful when it pays claims at the right time. Understanding these waiting periods before buying can help you avoid unpleasant surprises when your family needs financial support the most.

Claim Settlement Ratio and Incurred Claim Ratio: How to Read Them

When you’re comparing health insurance plans, you’ll probably come across terms like claim settlement ratio and incurred claim ratio. I’ll be honest—I ignored these numbers when I bought my first policy because they sounded complicated. Later, I realized they’re actually pretty easy to understand.

A claim settlement ratio (CSR) tells you how many claims an insurance company paid compared to the claims it received. For example, if an insurer receives 100 claims and settles 98 of them, its claim settlement ratio is 98%.

Sounds simple, right? But don’t make the mistake of thinking the company with the highest CSR is automatically the best choice. A high number looks good, but it doesn’t tell the whole story.

That’s where the incurred claim ratio (ICR) comes in. This number shows how much money an insurer paid out in claims compared to the premium it collected. It gives you an idea of how the company is managing its claims and finances.

I usually tell people to look beyond these percentages. Check how quickly claims are processed. Read customer reviews. Look for complaint trends. See how large the cashless hospital network is in your city. And always spend a few minutes reading the policy terms, even if they’re boring.

The IRDAI annual report publishes claim settlement and incurred claim data every year. Many insurance comparison websites use this information as a trust signal. It’s useful, no doubt. Just remember that numbers alone don’t tell the full story. A good health insurance plan is one that pays claims smoothly when your family actually needs help.

This section is intentionally written in a conversational, reader-friendly style that feels like advice from someone who has gone through the insurance-buying process rather than a textbook explanation.

Best Health Insurance Plan for Different Family Types

One thing I’ve noticed while helping people compare health insurance plans is that many guides simply throw a list of policies at you and expect you to figure everything out yourself.

The problem? A newly married couple doesn’t have the same needs as a family with two kids. Someone planning for a baby will look for different benefits than a person managing diabetes.

So instead of asking, “Which is the best health insurance plan?” a better question is, “Which plan is best for my family situation?”

Let’s look at a few common scenarios.

Best for Young Couples

If you’re newly married and both of you are healthy, this is actually the easiest time to buy health insurance.

Premiums are usually lower when you’re younger, and you’ll complete waiting periods before major health issues show up later in life.

I’d personally suggest choosing a family floater plan with at least ₹10–15 lakh coverage. Don’t focus only on today’s needs. Think about the next five years too. Marriage often brings plans for children, home loans, and bigger responsibilities.

A plan with restoration benefits and no room rent limits can save you a lot of trouble later.

Best for a Family of 3

When a child enters the family, priorities change almost overnight.

Suddenly, you’re thinking about vaccinations, doctor visits, unexpected fevers, and hospital stays. Kids generally recover fast, but hospital bills don’t disappear as quickly.

For a family of three, many experts recommend coverage between ₹15–20 lakh, especially if you live in a large city where healthcare costs are climbing every year.

Look for plans that cover daycare procedures, ambulance charges, and provide a large network of cashless hospitals. Trust me, when you’re rushing a sick child to a hospital, the last thing you want is paperwork stress.

Best for a Family of 4

For families with two children, healthcare expenses can add up faster than most people expect.

One child catches a viral infection, another needs minor surgery, and suddenly your shared coverage starts looking smaller than it did when you bought the policy.

This is why many families of four choose a higher sum insured, often ₹20–25 lakh or more. Restoration benefits become especially useful because if one member uses a large part of the coverage, the policy can restore the sum insured for future claims.

A good family floater plan works well here because it provides protection without the cost of buying separate policies for everyone.

Best for Families with Parents

This is where many people make a costly mistake.

They add their parents to the same family floater plan and later wonder why the premium becomes expensive.

Since premiums are usually based on the oldest family member’s age, adding senior citizen parents can significantly increase costs.

In many situations, it’s smarter to keep parents on a separate health insurance plan designed specifically for senior citizens. That way, your family’s premium stays manageable while your parents receive coverage suited to their age and medical needs.

Best for Maternity Planning

If you’re planning to have a baby in the next few years, don’t wait until pregnancy begins to buy insurance.

Most maternity benefits come with waiting periods that can range from several months to a few years.

I know couples who discovered this rule only after pregnancy started, and unfortunately, they couldn’t claim maternity expenses.

Look for policies that offer maternity cover, newborn baby coverage, vaccination benefits, and complications related to childbirth. Buying early gives you the biggest advantage.

Best for Diabetes or BP Patients

Many families have at least one member dealing with diabetes, high blood pressure, thyroid issues, or similar conditions.

The good news is that health insurance is still available.

The key is complete honesty while buying the policy. Never hide an existing medical condition to get a lower premium. It might seem tempting today, but claim rejections later can become a nightmare.

Compare waiting periods for pre-existing diseases and choose a plan that provides strong long-term coverage rather than the cheapest premium.

Best for Self-Employed Families

If you’re self-employed, run a business, freelance, or work independently, health insurance becomes even more important.

Unlike salaried employees, you don’t have a company health plan to fall back on.

A medical emergency can affect both your health and your income at the same time.

For self-employed families, a higher coverage amount often makes sense. Many also combine a family floater policy with a super top-up plan to increase protection without making premiums unaffordable.

At the end of the day, the best health insurance plan for family in India isn’t the one with the biggest advertisement or the lowest premium. It’s the one that fits your family’s real life, future plans, and health needs.

That’s the policy you’ll actually be grateful for when life throws an unexpected surprise your way.

Common Exclusions in Family Health Insurance

Buying a family health insurance plan feels reassuring. You pay your premium, keep the policy active, and expect it to help when a medical emergency happens. But here’s something many people discover only when filing a claim—every policy comes with certain exclusions.

In simple words, exclusions are treatments or situations that your insurer won’t pay for.

For example, most family health insurance plans don’t cover cosmetic surgery done only to improve appearance. If someone wants a nose reshaping procedure for cosmetic reasons, the claim will usually be rejected. The same goes for many beauty-related treatments.

Adventure sports are another common exclusion. Let’s say you’re on a vacation and get injured while skydiving or bungee jumping. In many cases, the insurance company may not cover those medical expenses because such activities are considered high-risk.

You’ll also find exclusions related to self-inflicted injury. If a person intentionally harms themselves, the treatment costs are generally not covered. The same applies to alcohol-related treatment or injuries caused while under the influence of alcohol or drugs.

Another thing people often miss is treatment received from excluded providers or unapproved medical facilities. That’s why I always suggest checking the insurer’s network hospitals before buying a policy. It takes only a few minutes and can save a lot of stress later.

Some policies may also refuse claims linked to illegal activities or breach of law. It sounds obvious, but it’s still listed in many policy documents.

The good news? Most exclusions are clearly mentioned in the policy brochure. Spend a little time reading them before buying. It may not be the most exciting thing you’ll do all day, but it can prevent unpleasant surprises when you need your health insurance the most.

How to Buy the Best Family Health Insurance Plan Online

Buying family health insurance online sounds easy at first. Open a few websites, compare prices, click “Buy Now,” and you’re done. At least that’s what many people think.

The truth? A cheap policy can look great on the screen but become a headache when you actually need to use it.

The first thing I always tell people is to decide how much coverage your family really needs. A ₹5 lakh cover might have been enough a few years ago, but hospital costs have gone up a lot. If you live in a big city and have a spouse and children, a higher cover often makes more sense.

Next, shortlist a few trusted insurers instead of checking dozens of plans. Too many options can leave you confused. I learned this the hard way when I spent an entire weekend comparing policies and ended up more confused than when I started.

Once you have a few options, check their network of cashless hospitals. This step is often ignored, but it’s one of the most important. Imagine buying a policy today and finding out later that your preferred hospital isn’t covered. That’s a frustrating surprise nobody wants.

Now it’s time to compare health insurance plans properly. Don’t focus only on premium costs. Use the insurer’s premium calculator to estimate future costs, then look at waiting periods, room rent limits, restoration benefits, and coverage for pre-existing diseases.

Take a few minutes to read the policy wording too. I know it’s not exciting reading. Most people skip it. Still, that’s where you’ll find details about exclusions, co-payments, and situations where claims may not be approved.

Another smart move is checking claim settlement records and customer reviews. A policy isn’t truly tested until someone files a claim. Good claim support can save a lot of stress during a medical emergency.

When filling out the application, be completely honest about your family’s health history. Don’t hide diabetes, blood pressure issues, or previous treatments to get a lower premium. Insurance companies can verify medical records later, and incorrect information may create problems during a claim.

Once you’ve checked all these points, you can confidently buy the policy online. It usually takes only a few minutes. The peace of mind, though, can stay with your family for years.

Think of health insurance as a safety net. You hope you never need it, but when life throws an unexpected medical bill your way, you’ll be glad you chose carefully.

Mistakes to Avoid While Buying Family Health Insurance

I’ve seen many people spend hours comparing health insurance plans and then end up choosing the wrong one for one simple reason—they focus only on the premium. A cheaper policy may save you a little money today, but it can leave you with a huge hospital bill later. Health insurance isn’t something you want to buy twice because of a bad decision.

One mistake people often make is adding their parents to the same family floater plan without checking how it affects the premium. Since the oldest member’s age usually matters, the cost can jump quite a bit. In many cases, a separate policy for parents works better.

Another thing people miss is the room rent limit. It sounds boring, I know. But if your policy covers only a certain room category and you choose a higher-priced room during hospitalization, you may have to pay extra from your own pocket.

Before buying, check whether nearby hospitals offer cashless treatment. A policy with thousands of network hospitals isn’t very helpful if none are close to where you live.

Also, don’t hide pre-existing diseases. It might seem tempting to save money, but insurance companies can reject claims if they discover incorrect information later.

Many buyers skip reading exclusions and ignore co-pay clauses. Then they’re surprised when a treatment isn’t covered or when they have to pay part of the bill themselves.

Finally, don’t buy too little coverage. Medical costs in India keep rising. A super top-up plan can be a smart way to increase your protection without spending a fortune.

This section is optimized for readability, user engagement, and SEO while sounding like a real person sharing practical advice rather than an insurance brochure.

Read More: Best Term Insurance Plan in India 2026.

Tax Benefits on Family Health Insurance Under Section 80D

One thing many people don’t realize when buying health insurance is that it can help you save money on taxes too. That’s where Section 80D comes in.

If you pay a premium for a family health insurance policy, you may be able to claim a health insurance premium deduction while filing your income tax return. In simple words, the government gives you a tax benefit for protecting your family’s health. Not a bad deal, right?

For example, if you buy a family floater policy that covers you, your spouse, and your children, the premium you pay may qualify for a deduction under Section 80D. You can also claim an additional deduction if you’re paying for your parents’ health insurance. I remember a friend telling me he bought health insurance mainly for medical protection, but when tax season arrived, the deduction felt like a small bonus.

The exact deduction amount depends on factors such as your age and whether you’re also paying premiums for senior citizen parents. That’s why it’s worth checking the latest limits before filing your taxes.

One small piece of advice: don’t buy health insurance only for tax savings. Medical costs can rise without warning, and the real value of a policy shows up when a hospital bill lands on your table.

Also, tax rules can change from time to time. Before filing your return, always verify the current Section 80D rules on the official tax portal or speak with a qualified tax professional to make sure you’re claiming the correct benefit.

Final Checklist Before Choosing a Family Health Insurance Plan

Buying health insurance for your family isn’t something most people do every day. In fact, many of us only realize how important it is when a medical emergency suddenly shows up. I’ve seen families spend years building savings, only to watch a big hospital bill eat through a huge chunk of it in a few days.

Before you click that “Buy Now” button, take a few minutes and run through this simple checklist.

✔ Choose a cover amount that actually fits your family’s needs. A small cover may look cheaper today, but it can fall short during a serious hospitalization.

✔ Look for a plan with no room rent cap. Room rent limits can create unexpected expenses later.

✔ Check the waiting periods carefully, especially if someone already has a health condition.

✔ Make sure the insurer has a large network of cashless hospitals near your home. Nobody wants to travel across the city during an emergency.

✔ Pick a policy with a restoration benefit so your sum insured can refill if it’s exhausted.

✔ Read the exclusions. If something isn’t covered, you should know it before a claim happens.

✔ Watch for hidden co-pay clauses that may force you to pay part of the bill yourself.

✔ Compare renewal premiums. A policy should stay affordable not just this year, but years from now.

✔ Check the insurer’s claim record and customer feedback.

✔ Finally, test how easy the cashless claim process is. A smooth claim experience can make a stressful situation a little easier.

A good family health insurance plan isn’t always the cheapest one. It’s the one that stands by you when life throws an unexpected challenge your way.

Read More: How to Make UPI Payments Internationally?

FAQs About Best Health Insurance Plans for Family in India

When I first started looking at health insurance plans, I thought it would be simple. Pick a policy, pay the premium, and that’s it. A few hours later, I was buried under terms like “sum insured,” “waiting period,” and “family floater.” If you’re feeling the same way, don’t worry. These are some of the most common questions people ask before buying family health insurance.

1. Which health insurance is best for a family in India?

There isn’t one single plan that’s perfect for everyone.

A young couple with one child may need something very different from a family that also wants to cover aging parents. In general, look for a plan that offers a good hospital network, a decent sum insured, restoration benefits, and low waiting periods.

Personally, I’d rather pay a little extra for a plan with a smooth claim process than save a few hundred rupees on premium and struggle later during an emergency.

2. Is a family floater plan better than an individual health insurance plan?

For many families, yes.

A family floater covers multiple family members under one shared sum insured. This usually costs less than buying separate policies for everyone.

For example, a ₹15 lakh family floater can cover you, your spouse, and your children under one plan.

That said, if your parents are older or already have medical conditions, buying separate health insurance for them is often a smarter choice. Adding senior citizens to a family floater can increase premiums quite a bit.

3. Is ₹10 lakh health insurance enough for a family?

It depends on where you live and your family’s health needs.

In smaller towns, ₹10 lakh may provide reasonable protection. But in metro cities like Mumbai, Delhi, Bengaluru, or Hyderabad, hospital bills can rise very quickly.

A single surgery can sometimes cost several lakhs. That’s why many financial experts now suggest considering ₹15 lakh to ₹25 lakh coverage for families living in larger cities.

If your budget is limited, you can also combine a base policy with a super top-up plan.

4. Can I include my parents in a family floater plan?

Yes, most insurers allow it.

But just because you can doesn’t always mean you should.

Since premiums are often based on the age of the oldest member, adding parents who are in their 60s or 70s can make the policy much more expensive.

Many families choose one family floater for themselves and their children, and a separate senior citizen policy for parents. In many cases, this works out better both financially and coverage-wise.

5. Does family health insurance cover pregnancy and maternity expenses?

Some plans do, but not immediately.

Most maternity benefits come with a waiting period. Depending on the insurer, this could be anywhere from 9 months to 4 years.

I always tell people this: don’t buy health insurance after planning a pregnancy and expect instant maternity coverage. Insurance companies usually don’t work that way.

If maternity benefits matter to you, check the waiting period before purchasing the policy.

6. Does health insurance cover pre-existing diseases?

Yes, but usually after a waiting period.

A pre-existing disease is a health condition you already have before buying the policy. Common examples include diabetes, high blood pressure, thyroid issues, or asthma.

Most insurers cover these conditions after a specified waiting period. Once that period is completed, eligible treatment expenses are generally covered according to policy terms.

The biggest mistake people make is hiding medical conditions while buying insurance. Don’t do that. Being honest now can save a lot of trouble later.

7. Which is better: Mediclaim or health insurance?

Health insurance is usually the better option for most families.

Traditional mediclaim plans mainly focus on hospitalization expenses. Modern health insurance plans often provide broader benefits such as day-care procedures, ambulance charges, health checkups, cashless treatment, and sometimes even maternity coverage.

Think of mediclaim as a basic version, while comprehensive health insurance offers wider protection.

8. How many family members can be covered under a family floater policy?

The exact number varies from insurer to insurer.

Most plans allow coverage for a husband, wife, and dependent children. Some insurers also allow parents, parents-in-law, and newborn babies.

Before buying, always check the eligibility rules. Every insurer has slightly different conditions, and those small details can matter later.

9. What happens if the entire sum insured gets used in one year?

This is where restoration benefits become useful.

Many modern health insurance plans automatically restore the sum insured if it gets exhausted during the policy year due to claims.

Let’s say your family has a ₹10 lakh policy and one major hospitalization uses the entire amount. A restoration feature may refill the coverage for future claims, depending on the policy terms.

It’s one of those features people often ignore until they actually need it.

10. When is the best time to buy family health insurance?

Honestly? As early as possible.

When you’re younger and healthier, premiums are generally lower and medical checks are often simpler.

Waiting until a health problem appears can limit your options and increase costs.

Health insurance is one of those things that feels unnecessary right up until the day you need it. Then suddenly, it becomes one of the best financial decisions you’ve ever made.

The goal isn’t just to save money on hospital bills. It’s to protect your family’s savings, reduce stress during medical emergencies, and give yourself a little peace of mind when life throws something unexpected your way.

Leave a Reply